Independent analyst Ryk De Klerk says it is understandable that Balwin needs more office space due to the scale of the launch of the Mooikloof Mega Residential City - a public-private partnership between Balwin Properties, the provincial government, and the City of Tshwane. File Image: IOL

ANALYSTS polled on the weekend backed JSE-listed Balwin Properties move to purchase an upmarket property in Melrose Arch, Johannesburg, with a price tag of R125 million for its new head office, in the wake of a social media backlash last week.

In a SENS statement last week, Balwin said there would be no initial constraint on its cash flow, and Investec Bank had approved the loan.

“The property is situated within the upmarket area of Melrose Arch, which is a rapidly-developing commercial and residential node... is highly visible from the M1 highway, and is perfectly situated to capitalise on the advertising opportunities,” it said.

Among reasons for the purchase, it said ownership of the property would give it better control over its operating expenses.

Balwin said it would initially occupy 2 500 squared metres of the gross lettable area of 7 341 square metres, with the balance available for lease by third parties at market-related rates.

“A number of Balwin’s top suppliers and professionals have shown strong interest in joining Balwin in the building and see this as a strategic business move. Balwin believes that the risk of having vacant office space is low,” it said.

Investors on fintwit, a vibrant community of investors on Twitter, were not impressed by the move.

The Passive Income Guy @hazelwood_dave, “So Balwin blows R125mn of scarce capital on an office building (unproductive asset) when office market is in dire straits & property values expected to fall. Thanks guys. One less company to research.”

The Finance Ghost @FinanceGhost did a twitter survey, “Balwin shareholders: how do you feel about the company taking on R125.8 million in debt to buy a flashy office in Melrose Arch?”. The result, “So it's unanimous then: Balwin is uninvestable once and for all?”

Was the negative sentiment based on Balwin’s balance sheet, or market sentiment on owning office property in the new, post-Covid-19 environment?

The REIT, valued at R1.7 billion, has seen its share price tank 32.56 percent in the past year, and is down 55.69 percent over five years.

In a trading update last month, Balwin said its core headline earnings per share was expected to increase by between 12 to 17 percent for the year to end-February, to between 80 and 83.6 cents per share, with its results expected out around May 6.

Meanwhile, the latest FNB Property Broker Survey, released earlier this month, showed that there was a “noticeable” increase in optimism about the future strengthening in sales activity in all three property classes, industrial, offices and retail, during the first three months of 2022.

John Loos, FNB’s property sector analyst, said: “We sense this surge in confidence has much to do with a feeling the Covid-19 pandemic risk is receding... and that 2022 is likely the year in which economic activity and human interaction normalise, whatever the ‘new normal’ might mean.”

Business Report decided to take the question to the experts.

Independent analyst Ryk De Klerk said, “In normal circumstances I would have questioned the lavishness of Baldwin Properties’ acquisition of a new HO in Melrose Park for R125 million”.

However, in October 2020, the Mooikloof Mega Residential City in Tshwane, Gauteng was launched. It is a public-private partnership between Balwin Properties, the provincial government, and the City of Tshwane. It is a huge project where residential property developments will eventuate to some 50 000 sectional title units.

It is, therefore, understandable that Balwin needs additional office space, De Klerk said.

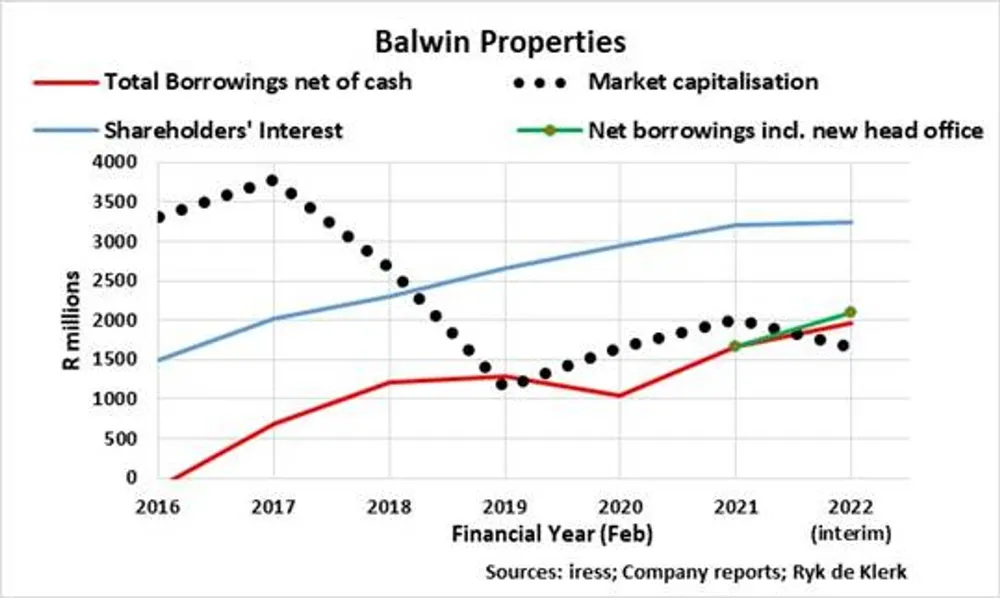

“The R125m should also be seen in perspective. The net asset value or shareholders’ interest amounted to about R3.2bn and at the halfway stage of the company’s 2022 financial year, while total borrowings net of cash amounted to R2.1bn. The purchase consideration will, therefore, increase net borrowing by about 6 percent and will be fully covered by the asset. What it means is that the net asset value or shareholders’ interest will be unaffected by the acquisition,” he said.

The property was highly visible from the M1 highway and is perfectly situated to capitalise on the advertising opportunities, especially in light of the company’s involvement in the Mooikloof development, he said.

“It is also interesting to note that since 2019, Balwin’s market capitalisation (issued shares times share price) tended to track the company’s total borrowings after taking into account cash and/or equivalents on hand. The company’s net worth is therefore 50 percent higher than the share’s market capitalisation. I rate the company as a 'buy',“ said De Klerk.

Shareholder activist Harry Smit said Balwin raised very valid points in their SENS announcement in that there would be huge savings in utilities, it would improve their corporate image and the aspect of free marketing.

The move also provided a diversified income stream, fall back income and closer inter relations with the firm’s major contributors to the business, he said.

Smit said market participants might misunderstand what HO costs represented.

“I am afraid, as they may look at it as lease expenses or utility bills etc. There are a lot more spokes involved that make the actual wheel turn. It’s not the cost of the building per se,” he said, adding that there should be a careful analysis of the basket that was identified as HO cost.

“Through my experience, the bulk of that lies in Human Resources and not physical assets or leases. The permanent staff quota... Their levels and their actual functions, and roles they fulfil, together with the return of investment the company gets from the expense its committing.

“So when we are talking about bloated HO expense we are talking staff, IT, advisers etc... For every five people you employ, you need one to check them. Even if they are doing the job of one... In a downturn like Covid-19 you are stuck with the same expense with one-third of the return,” he said.

Smit said the cost of advisers and executive remuneration needed to be closely monitored.

“In Balwin’s case, my question would be what are the costs and fees they pay consultants and deal teams to come up with the summary that this is a better move. I assure you if you scratch beneath the surface there are huge rewards and bonuses and fees behind the whole conclusion they have reached,” he said, adding, “and that’s where my problem as an activist would lie in this decision.”

BUSINESS REPORT