Solar power: 4 ways you can finance a system for your home, including renting one

|Published

Given the array of financing options that exist today, there is a need for more accessible financial cost comparisons. Picture: Colin McKay/Pixabay

The demand for alternative power solutions in South Africa has skyrocketed since 2021, but many people cannot afford to invest in such systems; luckily, if you don’t have the money to buy one outright, you can actually rent one.

Alternative energy systems range from simple fixes like Uninterrupted Power Supply (UPS) devices to more comprehensive solutions such as invertors, generators, and solar panel installation, with the latter being one that is very difficult to pay for upfront.

While solar has emerged as the most sustainable solution, there has not yet been a real, wide-scale shift to off-grid and grid-tied solar power, and the cost of it could be the reason.

Dominique dHotman, Head of ooba Solar, a platform that provides consumers with solar installation quotes for comparison and assists them in securing financing for their solar projects, says there are misconceptions about solar being a luxury reserved for the wealthy, but many people may not know that there is a wide array of solar financing options currently on offer.

“What’s more, solar solutions are generally priced on a sliding scale, depending on your power requirements.”

In fact, given the reduced barriers to entry that exist through solar financing, and the ease at which systems can be acquired, purchasing one for your home “should by now be a no-brainer”.

However, with the array of financing options available, there is a need for more accessible financial cost comparisons.

“Heightened demand brings opportunity. Here, it’s important that you compare all the options before simply signing on the dotted line to make sure that you understand the financial implications, and which option offers the biggest savings, in the long run.”

To illustrate his point, dHotman points to the escalating rental model in which consumers initially pay less than R2,000 per month.

“While this may seem to be the cheapest way to get access to a solar system, in the long run, it ends up costing you more.”

Solar power costs that are often over-looked

When comparing options, many homeowners fail to realise that solar systems are not entirely independent of the Eskom power grid, so you need to consider the total cost of ownership, which includes more than just the monthly financing instalment or rental fee.

This comprehensive cost accounts for a household's total electricity expenses, combining three unavoidable components:

- The financing instalment

- Eskom's standard monthly connection fee

- The residual usage of Eskom's power (measured in kWh) due to spikes in household consumption beyond the solar system's capacity or prolonged periods of low sunlight, or even just the less-than-ideal orientation of the house

The pros and cons of each solar power financing option

1. Asset finance

Both banks and non-bank lenders offer tailored loans for solar systems – covering up to 100 percent of the project’s financing, dHotman says.

- Pro: With a shorter pay-off period, you own the system – in full – after five years

- Con: Monthly instalments are the highest of the various financing options available, due to the shorter financing term and higher interest rate (around Prime +3.5 percent to 5.0 percent)

2. Government energy bounce back scheme

Introduced during the 2023 Budget Speech, this scheme operates as a loan guarantee for commercial banks seeking to provide loans to households for solar projects. Under this initiative, he explains that the National Treasury works with retail banks to provide concessionary funding, thereby lowering the cost of the solar loan to homeowners.

- Pro: While it operates similarly to asset finance, the interest rates are capped at a much lower level of Prime +2.0 percent and you own the system outright.

- Con: This scheme has a time limit given its bounce-back intention.

3. Home loan finance

The country’s major banks now offer solar financing through an existing bond or as an add-on to a new bond application.

- Pro: This option offers the most affordable monthly instalments as interest rates are often given at Prime or even a discount to Prime

“For Q3 ’23, ooba Home Loans achieved an average of prime -0.44 percent for our customers, so the rate discount is significant.”

- Con: An extended financing term means that the system will take longer to be paid off (up to 30 years, depending on the term of the bond)

4. Escalating rental model

Individuals choose a rental agreement, either as an equipment lease or as a power purchase agreement, with the monthly rental escalating annually, dHotman says.

- Pro: Lowest initial monthly instalments and the rental company will maintain the system

- Con: Monthly rental costs escalate each year, and the solar system remains the property of the provider after the contract ends. There are also de-installation fees, which will be payable if the homeowner wants to cancel the rental agreement or sells the property and can’t get the new owner to take over the rental agreement

Do the maths before you decide how to finance your solar power system

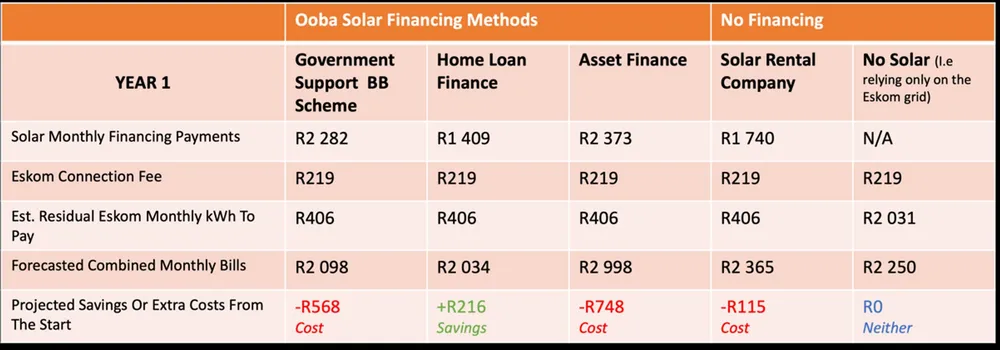

To compare the starting costs of each of the solar financing options on offer, he uses the example of a household in Cape Town, with an average monthly spend of R2,250 on municipal electricity (approximately 640 kWh per month).

“Typically, we look at a solar system that can supply around 80 percent of the household’s monthly power needs. One must, however, consider the monthly grid connectivity costs and the remaining 20 percent of the kWh’s still needed from Eskom or the municipality.”

With this disclaimer in mind, dHotman breaks down the year-one savings and monthly costs as follows:

“Here, home loan financing is the only financing option that offers initial savings upfront, which is a result of lower, inclusive monthly instalments that are calculated at a discount to Prime.

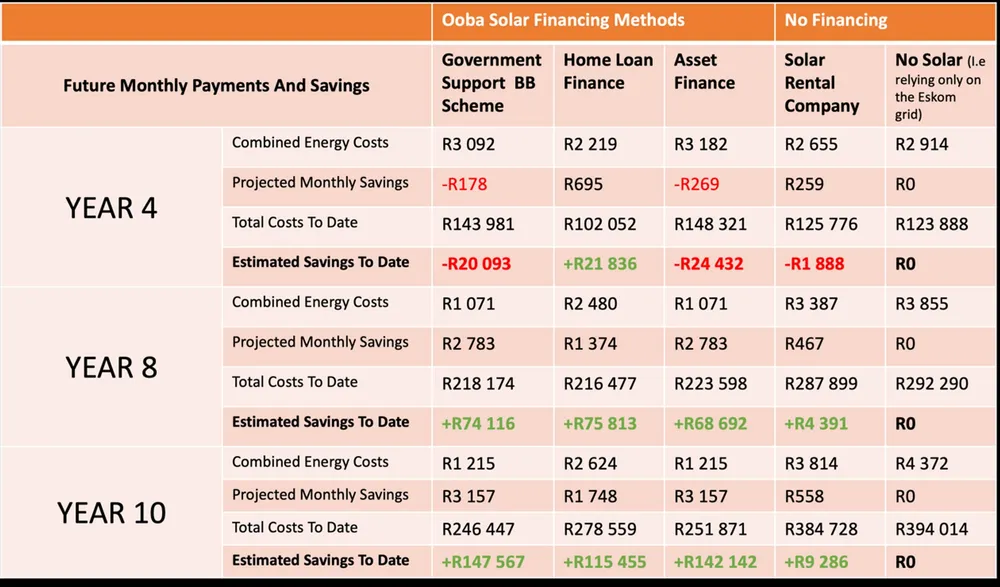

“Once these initial costings are established, we can look to the total costs and savings of the various solar financing options over a 10-year period.”

dHotman explains that home loan finance offers the greatest overall savings until year eight, when asset finance takes the lead. This is because asset finance instalments cease after year five, allowing for extra savings during the following three years.”

On the lowest end of the scale is solar rental, which equates to a saving of only R9, 286 over ten years. In comparison to the likes of asset finance, home loan finance and the government buy-back scheme, these savings are low, especially in light of the fact that the solar system doesn’t belong to you.

“Here, you miss out on all the benefits associated with asset ownership. Also consider that over the course of ten years, the amount you'll spend on renting will be more than double the cost of purchasing the system outright.”

IOL Business